Setting up a SIP feels like a responsible financial decision, and it is. But there’s a version of that decision that most investors make and never revisit: a fixed monthly amount, running indefinitely, untouched year after year. It looks like discipline. What it actually is, in most cases, is a plan that quietly falls behind the life it was supposed to fund.

A SIP calculator makes this visible in a way that’s hard to argue with. Run the same goal through it twice, once with a flat investment and once with an annual step-up, and the difference in projected corpus tells you everything you need to know about why your SIP amount should be moving.

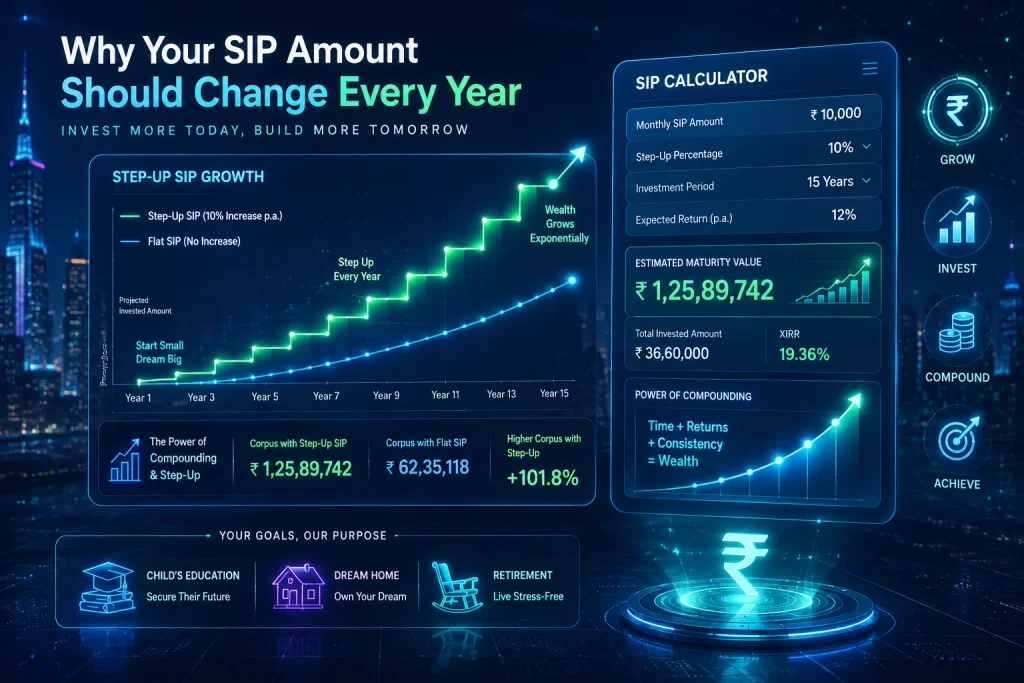

A Flat SIP is a Shrinking SIP

Here’s the thing about money that doesn’t move: the world around it does. Your expenses grow each year. The cost of your goals, whether that’s your child’s education, a home, or your own retirement, rises with inflation. A SIP amount that was meaningfully sized three years ago represents a smaller real commitment today, simply because the purchasing power of that monthly figure has declined.

This isn’t a reason to panic. It’s a reason to plan. A SIP calculator with a step-up feature lets you model exactly what happens when you increase your monthly investment by a fixed percentage each year, and the output consistently shows that even modest annual increases produce a materially larger corpus over time compared to a flat investment of the same starting amount.

The flat SIP investor isn’t doing something wrong. They’re just leaving compounding potential on the table by treating an investment decision as permanent when it was always meant to evolve.

What the Calculator Shows When You Compare

Pull up a SIP calculator and run two scenarios side by side. In the first, a fixed monthly amount is invested over fifteen years. In the second, the same starting amount with a modest annual step-up applied throughout. The difference in projected corpus at the end of that period is rarely trivial, and it becomes less trivial the longer the horizon extends.

What makes this comparison genuinely useful is what it reveals about the mechanics underneath. The step-up scenario benefits from two compounding forces working simultaneously: the growth of each rupee already invested, and the growth of each additional rupee added through the annual increase. Those two forces compound together over time in a way that no flat investment can replicate.

The SIP calculator doesn’t editorialise. It simply shows you the outcome of each approach with the same starting conditions. That objectivity is what makes it the right tool for this particular conversation with yourself.

Income Growth Makes the Step-Up Sustainable

One of the reasons people hesitate to commit to annual SIP increases is the assumption that it requires significant financial sacrifice each year. It rarely does because, for most investors, the step-up is designed to track income growth rather than exceed it.

If your salary or business income tends to grow each year, a proportional increase in your SIP simply keeps your investment in line with your earnings capacity. You’re not stretching further relative to your income; you’re maintaining the same proportional commitment as your financial situation improves. A SIP calculator lets you model this alignment directly, so you can see what a step-up percentage that mirrors your expected income growth actually produces over your chosen timeline.

This framing matters because it removes the psychological friction. The question isn’t “can I afford to invest more?” It’s “Should the same fraction of my growing income go toward my goals?” For most people, the honest answer is yes.

The Goals That Don’t Wait for You

Your investment goals have their own inflation. School fees rise. Property values move. Healthcare costs increase year on year in ways that general inflation figures often understate. A retirement corpus calculated today needs to account for what that money will actually buy twenty years from now, not what it buys today.

When you use a SIP calculator for goal-based planning with a step-up applied, you’re building an investment strategy that at least acknowledges this reality. You’re not assuming that a fixed monthly commitment today will be sufficient to meet a goal whose cost is actively rising. That’s a more honest basis for planning, and a more resilient one.

The investors who reach their goals aren’t always the ones who started with the most. They’re the ones who adjusted as they went.

Conclusion

A SIP calculator won’t tell you what to do. But it will show you, with clarity, what different choices produce over time, and the gap between a flat SIP and a stepped-up one is one of the most instructive comparisons it can make.

Your income grows. Your goals grow. Your SIP should too. The calculator simply makes the case better than any argument could.